Filter By Market

U.S. commodities platform that traded industrial hemp shuts down as investor pulls back

HempToday U.S. analyst and commodities platform PanXchange, which operated in hemp and other sectors, has discontinued operations, according to the ...

Read More

Read More

PanXchange Carbon Credit Market to Integrate with the Hedera Blockchain

DENVER, Aug. 28, 2023 /PRNewswire/ -- PanXchange, which offers a vertically integrated carbon exchange program for nature-based solutions today announced ...

Read More

Read More

PanXchange on Hedera

Blockchain technology is breaking barriers in many industries, so it shouldn’t come as any surprise that it’s currently being utilized ...

Read More

Read More

Carbon Projects on Leased Land

Please note that this article does not constitute legal advice. There is often confusion regarding the execution of carbon offset ...

Read More

Read More

Key Takeaways from Microsoft’s FY23 Carbon Briefing Paper

Microsoft issued its 2023 FY briefing paper this month. The document provides strong guidance on voluntary market trends, as Microsoft ...

Read More

Read More

Bezos Earth Fund – Data Progress Needed to Advance Climate Smart Agriculture

The Bezos Earth Fund, in partnership with Stanford Law School, published a report on the data progress needed to advance ...

Read More

Read More

2023 WALL STREET GREEN SUMMIT

2023 WALL STREET GREEN SUMMIT Decarbonization and CarbonTech 2.0 Morning Webinar on Monday March 13th on ESG Reporting and Investing ...

Read More

Read More

PanXchange on Hedera – Gossip About Gossip

PanXchange Founder/CEO Julie Lerner Julie Lerner, CEO and founder of PanXchange was welcomed to 'Gossip About Gossip', powered by Hedera ...

Read More

Read More

Agricultural Carbon Credits- Listen to the Farmers

Nature-based solutions are one of the most scalable opportunities to address climate change, but farmers have become increasingly skeptical about ...

Read More

Read More

2022 in Review and 2023 Predictions

Thankfully, 2022 is over, and we made it through with our questionable sanity intact. The new year is both a ...

Read More

Read More

5 Hemp Projects in USDA Climate Smart Commodities 2nd Announcement

By Jean Lotus, PanXchange Blog The US Department of Agriculture dropped the second tranche of the total $3.5 billion Climate ...

Read More

Read More

Rental Contracts and Partial Credit for Temporary Carbon Storage

PanXchange Blog Arguably, the trickiest part of the burgeoning voluntary carbon market is not measuring the carbon sequestered, but ensuring ...

Read More

Read More

Industrial Hemp Grower’s Digest • Julie Lerner with PanXChange

Industrial Hemp Growers Digest Podcast Julie Lerner took her knowledge of the agricultural trading and supply chain business and has ...

Read More

Read More

Hemp Production Down by Almost 50 Percent — But Why?

HEMP Hemp Production Down by Almost 50 Percent — but Why? AMBER TAUFEN NOVEMBER 2, 2022 5:32AM Colorado's hemp farms ...

Read More

Read More

U.S. Hemp Harvest Expected to Fall by Nearly Half

The 2022 hemp harvest in the U.S. is expected to shrink by nearly half this year, falling from roughly 36,925 ...

Read More

Read More

Accurate Hemp Data Requires Collaboration

From Lancaster Farming The hemp industry has been waxing and waning for the last several years, gaining traction in some ...

Read More

Read More

CA Wetlands Sequester CO2 in Peat

Photo courtesy USDABy Alex Maleshko, PanXchange Blog Wetlands are one of the most potent nature-based systems on land that sequester ...

Read More

Read More

Biden-Harris Administration Announces Roadmap for Nature-Based Solutions to Fight Climate Change

Nature-based solutions include protection or conservation of the natural environment, which can slow climate change by capturing and storing carbon ...

Read More

Read More

Cows, Hemp and THC — Facts not Hype

Headlines in November raced with news that cows exhibited intoxicated behavior after being fed high-THC “hemp silage” by German food ...

Read More

Read More

Hemp’s Role in US Marijuana Price Crash

PanXchange Blog Analysis By Seth Boone, PanXchange US recreational and medical marijuana markets have expanded significantly with 19 states now ...

Read More

Read More

Hemp Soil Remediation Part of $10 Million Grant in Decatur, IL

Jean Lotus, PanXchange The city of Decatur, IL has included planting acres of industrial hemp for soil remediation and erosion ...

Read More

Read More

Minnesota DOT Explores Hemp for Erosion Control

A pilot program to develop hemp-based erosion control materials for the Minnesota Department of Transportation is in its second year ...

Read More

Read More

Value the Seed Campaign

The "Value the Seed” policy reform initiative, when adopted, will enable U.S. hemp farmers who use and plant Certified seed ...

Read More

Read More

Hemp-Lime Approved in US Building Codes

Hemp building materials were officially approved in the model US residential building code at a public hearing overseen by the ...

Read More

Read More

Hemp Scores 2 Grants in USDA Climate Smart Commodities Awards

The United States Department of Agriculture included two significant hemp projects, one tied to carbon sequestration, in the first list ...

Read More

Read More

Hemp Animal Feed Too Vital to Ignore in US

The industrial hemp plant offers a long list of potential animal feed inputs that could be readily derived from hemp ...

Read More

Read More

5th Annual New Directions in Commodities Research Symposium

5th Annual New Directions in Commodities Research Symposium PanXchange Founder/CEO Julie Lerner Julie Lerner, CEO and founder of PanXchange will ...

Read More

Read More

New West Genetics: Blazing a Genomic Trail for Hemp

PanXchange Blog New West Genetics, an international leader in hemp seed genetics, was founded in 2014 by Rich Fletcher and ...

Read More

Read More

D8 Market Stabilizes Prices for Bulk Hemp Cannabinoids

By PanXchange A Ninth Circuit US Court of Appeals ruled May 19 that delta-8 THC products are federally legal according ...

Read More

Read More

Deregulating and Destigmatizing Hemp Fiber and Grain

Many hurdles stand in industrial hemp’s path to becoming a common rotational crop in the United States. Expensive testing, licensing, ...

Read More

Read More

Midwest iHemp Expo. Lansing, MI. May 20-21, 2022

Seth Boone, VP of Hemp, will be presenting Friday and Saturday at the Midwest iHemp Expo. Friday's presentation will focus ...

Read More

Read More

The 6 Core Tenets for CEOs

In 2018, I had the great honor of being recognized by the Denver Business Journal in their Most Admired CEO ...

Read More

Read More

PanXchange and IND Hemp, 1 of the top 287 Selected to Move to Next Stage of Carbon Removal XPRIZE

We are proud to have advised The Hemp Team (IND Hemp) with project management, technical, and commercial content for their ...

Read More

Read More

PanXchange Carbon Credit Course: Go to Market Strategy

PanXchange Carbon Credit Course: Go to Market Strategy In this webinar, PanXchange covered the following areas: - Executing a carbon ...

Read More

Read More

PanXchange Carbon Credit Course: Go to Market Strategy

PanXchange Carbon Credit Course: Go to Market Strategy In this webinar, PanXchange covered the following areas: - Executing a carbon ...

Read More

Read More

Hemp & Animal Feed: PanXchange Releases Analysis in First of Three Industry Reports

October 14, 2021 Denver, CO. PanXchange today announced the release of its white paper on the many applications of hemp ...

Read More

Read More

Barchart Webinar: Explore PanXchange’s latest Hemp and Animal Feed Report

Join us for an exclusive webinar taking place Thursday, October 21st at 2pm CST with Barchart’s Senior Account Executive, Ryan ...

Read More

Read More

Southern Hemp Expo 2021

This is the audio from the 2021 Southern Hemp Expo panel discussion about carbon credits featuring our VP Seth Boone ...

Read More

Read More

Forbes 50 Over 50

Julie Lerner is one of 50 women who are shaping the future of finance, fueling high-growth businesses and forging a ...

Read More

Read More

Hemp Industry Must Emulate Mature Markets

Love of the hemp plant does not guarantee its success. But in order for a crop to be economically viable, ...

Read More

Read More

What to Make of the FSA Hemp Planted Acreage

The Farm Service Agency (FSA) released their initial August planting report yesterday which estimates hemp plantings across all applications at ...

Read More

Read More

Hemp Fails the Economic “Taste Test” as an Alt-Meat Additive

PanXchange examines a case study of hemp protein use in retail food products by a company named Craft Foods, and ...

Read More

Read More

PanXchange Hemp Market Report April 2021

Using methods that are both creative while remaining scientific and methodical, PanXchange has managed to find short-term variables that can ...

Read More

Read More

UT to host free hemp webinar

See PanXchange's Vice President of Business Development, Seth Boone's comments in the 2021 Hemp Market Webinar ...

Read More

Read More

Between Two Hemp Stalks: Annie Rouse & the Issue of 1% THC in Hemp

Enjoy a transcript of a conversation between PanXchange’s CEO, Julie Lerner, and Annie Rouse, Co-founder of OP Innovates, Overcome, Hemp ...

Read More

Read More

Let’s Go Get High On Hemp!

Will transforming hemp-based CBD into mildly psychoactive Delta-8 THC save industrial hemp production? It’s complicated ...

Read More

Read More

The Hard Truth: Delta 8 Sales Needed to Work Through a Million Lbs of Oversupply

Today, the PanXchange team has found that over millions of pounds of oversupply have accrued since the 2019 crop and ...

Read More

Read More

Hemp trademark lawsuit involving Denver firm may signal future fights in burgeoning space

PanXchange founder and CEO Julie Lerner told DBJ that she sees the lawsuit as frivolous and an attempt to drain her company ...

Read More

Read More

Caution replaces euphoria as hemp event attendees wrestle with changing market

The CBD/hemp markets, both in finished goods and on the supply side, are in a state of transition ...

Read More

Read More

Industrial Hemp Carbon Footprint

CSU researchers have determined that growing one ounce of the hemp is equivalent to burning up to 60 liters of ...

Read More

Read More

In Illinois, Farmers Begin Examining Fiber Market’s Potential

There's a growing interest among farmers and a certain degree of demand among consumers for hemp fiber products. What's needed ...

Read More

Read More

PanXchange Hemp Market Report – March 2021

A podcast with Julie Lerner, Founder & CEO, PanXchange discussing trademark infringement, smokable hemp, and Delta-8-THC. PanXchange CEO, Julie Lerner, ...

Read More

Read More

2021 to hemp farmers: Stop chasing CBD, try this instead

Hemp and CBD are a double-edged sword. One of the biggest detriments to the hemp industry that could’ve occurred is ...

Read More

Read More

How Much US Farmland Should Be Dedicated to Hemp Crops?

Operating under the assumption an average bottle of CBD contains 1,500mg, some industry leaders believe even fewer acres will be ...

Read More

Read More

Cannabis to Face Big Policy Issues in 2021

There was widespread disappointment with a report authored by FDA Commissioner Stephen Hahn and published in January titled Use and Safety ...

Read More

Read More

How Much U.S. Farmland Should Be Dedicated to Hemp Crops?

Subsequently, U.S. acreage dedicated to hemp crops in 2020 fell by nearly 60 percent ...

Read More

Read More

Hemp CBD oversupply has farmers questioning their 2021 strategy

Here’s a numbers game for you. Guess how many acres of hemp the entire CBD business world needs to supply ...

Read More

Read More

PanXchange Launches Crowdfunding Campaign to Protect Itself from Competitor’s Trademark Abuse

PanXchange, Inc, the market structure solution for physical commodities, today launched the first $50,000 tranche of a fundraising campaign to ...

Read More

Read More

Where Hemp Fiber Could Find a Fit in 2021

Excitement is brewing around hemp’s potential as a substitute for various products. As the 2021 planting season draws nearer, COVID-19’s economic ...

Read More

Read More

Will the Smokable Hemp Market Go Up in Flames?

Hemp prices have fluctuated dramatically over the past two growing seasons, as hemp farmers know all too well. The biomass ...

Read More

Read More

Meet the winners and finalists: 20th CTA APEX Awards

Colorado Technology Association recognized those who excel in the tech industry at its 20th annual APEX Awards virtual awards program, ...

Read More

Read More

Opinion: Hope is not a strategy, so stop tolling

Basing the multibillion-dollar, pie-in-the-sky forecasts for the U.S. addressable market for CBD on retail shelf prices disturbs me ...

Read More

Read More

CBD Prices Languish as KSU Studies Using Hemp in Feed

It has been quiet lately in hemp country – which, since the 2018 Farm Act, of course, includes all 50 ...

Read More

Read More

APEX Awards CEO of the Year Award Overview

Colorado Technology Association Watch to hear from the three finalists, including Julie Lerner, for the APEX Awards CEO of the ...

Read More

Read More

CQG Releases New PanXchange Widget on CQG Desktop

New Offering Provides Direct Access to Premium Benchmarks and Analysis Content for Hemp, Frac Sand, East African Commodities CHICAGO / ...

Read More

Read More

Hemp Industry 2021 Opportunities Report

Let’s Talk Hemp is a publication of Colorado Hemp Company (a division of We Are For Better Alternatives) focused specifically ...

Read More

Read More

Nucleus195 TV | A look ahead 2021

We spoke with the Nucleus195 content providers and friends for their thoughts on the markets for 2021. Happy holidays and enjoy! Stay ...

Read More

Read More

Hemp Grower Editors Pick Their Favorite Stories from 2020

As this incredibly tumultuous year comes to a close, so does another year of hemp features and b2b journalism at Hemp ...

Read More

Read More

Hemp’s Future Twists and Turns Go Beyond Current CBD Marketplace

Our friends at PanXchange have included, along with their usual invaluable market insights, a year’s-end forecast to get us started ...

Read More

Read More

Interest in Hemp Fiber Rising as Farmers Look to 2021

In 2020, cannabinoid production undoubtedly continued to steal the hemp show. According to a recent survey by market analytics firm ...

Read More

Read More

PanXchange(r) Hemp: Benchmarks and Analysis released today with its Second Annual Supply and Demand Outlook

DENVER, CO, UNITED STATES, December 17, 2020 /EINPresswire.com/ -- The December 2020 edition of the PanXchange®: Hemp Benchmarks and Analysis was released ...

Read More

Read More

A Patchwork of Regulations: Hemp Pilot Programs Here to Stay Through 2021

This year was poised to be a turning point for the hemp industry as regulations set forth by the Agricultural ...

Read More

Read More

Julie Lerner, CEO of the Year Finalist for the 20th Annual APEX Awards

This year’s APEX Awards will be a week-long digital celebration of the leaders and companies elevating Colorado tech to new ...

Read More

Read More

2020 is the Year of Cannabis Legalization, but that Doesn’t Make it a Commodity

November 3, 2020 was a clear win for the cannabis industry. Five states passed legislation that legalized some form of ...

Read More

Read More

cmdty Pricing Network Interview – PanXchange

Hear from Julie Lerner, Founder and CEO of PanXchange, the leading benchmark price provider in US Hemp and the defacto ...

Read More

Read More

E-Frac Fleets, A Future of Promise or Peril?

An interesting advancement in technology in the oilfield services space is the NOV Ideal e-frac fleet. NOV’s e-frac fleet is ...

Read More

Read More

The Hemp Industry Has Room To Grow

As the third nationally legal industrial hemp crop hits the market, it is clear that American producers, consumers, merchants and ...

Read More

Read More

PanXchange’s Year-End Symposium

On December 18th at 10:30 am MST, after the December 17th PanXchange Hemp®: Benchmarks & Analysis report is published, PanXchange ...

Read More

Read More

PanXchange Powers Through Pandemic with Award-Winning CEO Julie Lerner

Before Denver’s population boom several years ago, Julie Lerner, CEO and Founder of PanXchange, the leading benchmark price provider in the US ...

Read More

Read More

PanXchange: Hemp Benchmarks and Analysis – Web Session: November 2020

On Wednesday following the distribution of PanXchange® Hemp: Benchmarks and Analysis, the Hemp team will be recording an online webinar ...

Read More

Read More

Fourth Annual State of the Cannabis Industry Conference – Demystifying Hemp & CBD

On October 29, 2020, Burns & Levinson hosted its Fourth Annual State of the Cannabis Industry Conference, with nearly 200 ...

Read More

Read More

Proposing a Standard Nomenclature for Cannabis and Hemp Derivatives

The lack of standard terminology in the cannabinoid industry is a barrier to communication in business and science. At the ...

Read More

Read More

Women in Finance Awards Finalists Announced – Julie Lerner

Markets Media Group is pleased to announce finalists for the 6th Annual Markets Choice Awards: Women in Finance event, to ...

Read More

Read More

Hemp Production Normalizes (Not Normlizes)

Hemp farming is experiencing normal growing pains. We can see the industry’s maturation in the evolution of the legal, commercial ...

Read More

Read More

What Happens When Cannabis Becomes A Commodity?

I’m often asked to comment on whether or not cannabis will ever truly attain the status of a commodity. While ...

Read More

Read More

COVID-19 vs. PanXchange, a Trading & Benchmark Pricing Platform for Physical Commodities

Julie Lerner: Of course, this pandemic is a tragedy that has brought sudden hardship and loss to many worldwide. While I ...

Read More

Read More

Hemp Acres Prices Down 2020

The Mosbys and Riders of Eldorado, Ill., took the 3 acres of hemp they harvested in 2019 down to 2 ...

Read More

Read More

Majority of US vegetable growers steering clear of hemp production for now

Hemp Industry Daily Vegetable growers across the U.S. weren’t among the traditional farmers heavily diversifying into hemp production in 2020 ...

Read More

Read More

Barchart and PanXchange Announce Strategic Partnership

CHICAGO, IL - October 29, 2020 - Barchart, the leader in commodity data, jointly announces a new strategic partnership with PanXchange, the leading ...

Read More

Read More

Prices for grain, hemp stalks to be tracked in USA

U.S. commodities trading platform PanXchange said it will begin to track prices for hemp grain and stalk for the USA ...

Read More

Read More

PanXchange Expands its Suite of US Industrial Hemp Benchmarks

PanXchange will begin issuing the first and only US benchmark prices for Hemp Grain and True Hemp beginning with its ...

Read More

Read More

PanXchange and Julie Lerner are both named a 2020 Benzinga Fintech Listmaker Finalists!

On Nov. 10th, 2020, PanXchange and Julie Lerner will be named a Benzinga Global Fintech Listmakers and recognized as Best ...

Read More

Read More

Hydraulic Fracturing: A Series of Events in Key Oil Producing States

While hydraulic fracturing activity is, in some cases, governed federally (such as when conducted on federal land), but based on ...

Read More

Read More

The John Lothian News Daily Update – 10/15/2020

It is with sadness I report to you the death of longtime SG/Newedge technology executive Ed Netter. Here is the ...

Read More

Read More

Between Two Hemp Stalks

Lerner: Often, during industrial hemp harvests, many farmers share with PanXchange their frustration of wasting hemp hurd, so I’m glad ...

Read More

Read More

Farm Bill Extension Leaves Opportunities and Hurdles For the Hemp Industry

2020 has been both a year of dynamic transition and reset for the hemp industry. The market is experiencing fundamental ...

Read More

Read More

Industrial Hemp Products Are More Than Just CBD

The health care market has recently been flooded with a wide variety of products made with industrial hemp extracts. The ...

Read More

Read More

HIA Board of Directors Gains Two New Members

Hemp Industries Association VANCOUVER, Washington – The Hemp Industries Association announces the appointment of two new members to its Board ...

Read More

Read More

Healthy Outlook For 2020 Hemp Production

John Lothian News There is some good news about industrial hemp production buried in PanXchange’s September 2020 report, Hemp: Benchmark ...

Read More

Read More

Fire On The Mountain: The Fight For West Coast Cannabis Growers

As if 2020 hasn’t piled on enough, California and Oregon have been ravaged by wildfires for the last two months ...

Read More

Read More

Overhyped hemp? Amid major price drop, and a big bankruptcy, Kentucky hemp farmers feel burned

Ohio Valley ReSource John Fuller is waiting for another farmer he’s never met before to talk about a situation he ...

Read More

Read More

Almond, Soy, Oat, and Even Hemp Milk!

Over the last few years, non-dairy milk has been popping up all over coffee shops and grocery store shelves. This ...

Read More

Read More

PanXChange hemp data reports now available through the Nucleus195 marketplace

Nucleus195 is pleased to announce that PanXchange has joined its ever-growing list of content and data providers network. “PanXchange is ...

Read More

Read More

Severe Weather’s Effect on Biomass & Smokable Flower Supply

PanXchange Blog The American hemp farmer can’t seem to catch a break between the two significant problems they face: legislative ...

Read More

Read More

Federal hemp underreporting is a huge problem for the industry – but there’s still time

Hemp Industry Daily Federal numbers on nationwide acres in certain crops are always a hot topic in the agri-community. But ...

Read More

Read More

Canadian-US Hemp Grain Market is Heating Up

Before CBD was a product category, hemp grain, oils, and protein were in high demand. Driven by consumer demand for ...

Read More

Read More

Hemp Production in the Western U.S.

Progressive Dairy In an industry that’s changing as rapidly as a landslide in an earthquake, no matter what figures presented ...

Read More

Read More

Liberty acquires Schlumberger’s Hydraulic Fracturing Division (OneStim): The Frac Sand Perspective

In one of the most monumental transactions in the hydraulic fracturing industry to date, Schlumberger (one of the largest oilfield ...

Read More

Read More

Why Reporting Your Hemp Acreage to the FSA Matters

We highlight some of our conversations with industry professionals who explain the many ways that underreporting hurts the industry as ...

Read More

Read More

Hemp Prices: “I’ve Fallen and I Can’t Get Up”

The August 2020 PanXchange® Hemp: Benchmarks and Analysis was published last week by our friends at PanXchange. Now, at the ...

Read More

Read More

Hemp-Filled Public Urinals

The hemp industry has praised the hemp market value for its versatility to be molded and used in hundreds of ...

Read More

Read More

The 7 Stages of Commodity Market Evolution

The year 2019 will be remembered as a watershed year for physical commodities. The 120 million-ton U.S. proppant market felt ...

Read More

Read More

Price slump saps Texas hemp crop, but optimism still blooms

By early October, Aaron Owens anticipates that the young hemp plants he’s cultivating on two acres just south of Dripping ...

Read More

Read More

J.P. Morgan Center for Commodities: Industry Advisory Council

The J.P. Morgan Center for Commodities' industry partners are key entities in the commodities area, including representatives from banking and ...

Read More

Read More

What is Delta 8 THC?

Delta 8 THC (D8) is a major cannabinoid present in both hemp and cannabis, mimicking the psychoactive effects of its ...

Read More

Read More

USDA: Hemp farmers didn’t lose enough money to receive coronavirus assistance

Hemp Industry Daily Federal agriculture officials have determined that hemp farmers don’t qualify for a $16 billion fund designated for ...

Read More

Read More

FSA’s August Crop Report – What’s Missing?

The USDA Farm Service Agencies (FSA) Crop Acreage Report on industrial hemp left the PanXchange’s hemp team scratching our collective ...

Read More

Read More

2020 DBJ Outstanding Women in Business: Julie Lerner, Small Business Leader Winner

Denver Business Journal We are so honored to announce that Julie Lerner won the category of Small Business Leaders at Denver Business Journal's Outstanding ...

Read More

Read More

Cannabis Weekly: CBD Supply Seen Shrinking as Farmers Flee Hemp

U.S. farmers appear to be fleeing the hemp market after a rush last year to meet over-hyped CBD demand resulted ...

Read More

Read More

Hemp Prices Stagnate; Hempcrete Gets Debunked

PanXchange’s July hemp benchmark report was published on Wednesday. If you have been following this space you will not be surprised ...

Read More

Read More

Hemp Transparency: Where Does the Hemp Plastic Go?

Over the last few years, hemp has received plenty of fame for its potential environmental impacts that come from its ...

Read More

Read More

Hemp’s Potential in the Animal Feed Market

Hemp has all the makings of a competitive ingredient in animal feed, but the industry has significant legislative hurdles to ...

Read More

Read More

DBJ’s 2020 Outstanding Women in Business Finalists

Meet the finalists, including Julie Lerner, our CEO, and Founder, in DBJ's 2020 Outstanding Women in Business awards program ...

Read More

Read More

The Frontier of Rig Platform Robotics

Rig platforms are often in remote locations with harsh, dangerous environments and limited resources for human operators on site. That ...

Read More

Read More

Greenhouse Hemp Market Update with PanXchange’s RJ Hopp

Widely viewed as a primary source for market reports and intelligence in the hemp industry, PanXchange (Denver, CO) Director of Hemp Market, ...

Read More

Read More

The Hoban Minute – 59 | Panxchange Julie Lerner | What Is A Commodity?

The Hoban Minute Bob and Eric sit down with CEO of Panxchange, Julie Lerner to discuss the basics of how ...

Read More

Read More

Oil and Gas Onshore: Alex Meleshko, Manager of Frac Sand at PanXchange

In this episode, Justin sits down with Alex Meleshko, Manager of Frac Sand at PanXchange to discuss Commodity Trading and ...

Read More

Read More

3 Takeaways From ‘The Forward Contracting Hemp In An Oversupplied Market’ Webinar

Last week, PanXchange hosted a webinar titled “The Forward Contracting Hemp in an Oversupplied Market.” The session, which will soon be available ...

Read More

Read More

Hemp Enters Growing Season Against Backdrop of Moribund Prices

No one will be surprised to learn that the price of CBD-hemp has stayed in the basement, resisting any pull ...

Read More

Read More

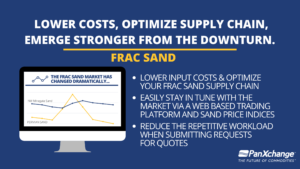

Lower Costs, Optimize Supply Chain, Emerge Stronger from the Downturn

During periods of low oil prices, industry players commonly perform “look back” exercises to lower their costs and optimize their ...

Read More

Read More

‘This is your moment:’ 5 tips on hemp investing from top analysts

Investors looking for a cannabis investment with less risk than the THC market have been snapping up hemp investments. But ...

Read More

Read More

The Oilfield Equipment Market

In North Dakota, a used Caterpillar Oil swabbing rig which would cost over $500,000 new was sold for $27,500 (a ...

Read More

Read More

Hemp Horse Bedding – A Look Into the Florida Market

Driving north on i75, from Tampa to Tallahassee, is what some consider to be a boring drive. Views solely consist ...

Read More

Read More

PanXchange Hemp Market Report Podcast – June 2020

We caught up with RJ Hopp, Director of Hemp Markets at PanXchange once again to talk about the wild, wild, ...

Read More

Read More

Forward Selling Hemp in an Oversupplied Market Webinar

This webinar will feature Julie Lerner, Kim Harris, and Bob Hoban all accredited professional and business leaders in the hemp ...

Read More

Read More

Oil and Gas Technology – Efficient, Flexible & Scalable

Advancements in technology are best implemented under the correct context, and in oil and gas, a significant talking point with ...

Read More

Read More

CBD Suffers From Hangover as Planting Season Begins

The prices for unprocessed hemp for CBD (CBD biomass) and for distilled CBD have consolidated at low levels, according to ...

Read More

Read More

Why Aurora’s Expansion Into the U.S. Market Really Isn’t All That Exciting

In recent weeks, Aurora Cannabis stock has seen new life. It all started with the company releasing its third-quarter 2020 results ...

Read More

Read More

Lobby group seeks USDA changes on hemp assistance

Citing a precipitous downturn in hemp commodity prices, the U.S. Hemp Roundtable has written to federal agriculture authorities seeking a change to ...

Read More

Read More

Be a Price Maker, Not a Price Taker

Virtually every physical commodity market (even specialty markets such as industrial hemp and specialty sand for the energy industry) is currently experiencing a significant oversupply scenario. ...

Read More

Read More

PanXchange Hemp Market Report Podcast

We talk with RJ Hopp, Director of Hemp Markets about the hemp market fluctuations, declining hemp licenses, and the outlook ...

Read More

Read More

Effects of the Ethanol Market on CBD Industry

Financial and commodity markets, regardless of the industry, have changed due to the outbreak of COVID-19. ...

Read More

Read More

Painting a Picture: The Perils of US Shale

The team at PanXchange wanted to shed some perspective on how calamitous of a downturn this has been for the ...

Read More

Read More

The Hemp Marathon

These rulings continue, despite a federal decision to de-schedule hemp as a controlled substance and forty-seven individual states adopting some ...

Read More

Read More

Hydraulic Fracturing: Using Machine Learning to Get the “Right Recipe”

The “tried and true” way to assess the performance of an oil well is to compute the total cost per ...

Read More

Read More

CBD Demand High, Fewer CBD-Hemp Acres Expected in Key States in 2020

As part of our evolving coverage of all aspects of the cannabis business, John Lothian News is passing on information ...

Read More

Read More

Tracking Hemp Data & Analytics

2020 is a year that no one saw coming, such is the case throughout the projected hemp industry, PanXchange is ...

Read More

Read More

US Crude Oil Supply and Demand – Latest Developments and Drivers

Below are some recent talking points on both the demand and supply side for crude oil markets to think about ...

Read More

Read More

JPMorgan Commodity Center Symposium: A White Paper on the Seven Stages of Commodity Market Evolution

Ms. Julie Lerner, Chief Executive Officer, PanXchange, participated in the commodity industry panel during the JPMCC’s 3rd Annual International Commodities ...

Read More

Read More

The Slow, Painful Post-COVID Oil Price Recovery

An interesting argument was inspired by popular energy analyst and engineer David Ramsden-Wood, who I credit with initially addressing this ...

Read More

Read More

![Generic Manufacturing: The Buried Treasure Beneath the [Frac] Sand](https://panxchange.com/wp-content/uploads/2020/04/Image-from-iOS-300x191.jpg)

Generic Manufacturing: The Buried Treasure Beneath the [Frac] Sand

Frac sand suppliers have struggled in the current market environment. Crude oil prices have crumbled amid a major oversupply (especially ...

Read More

Read More

Offshore Crude Oil Storage Trading and Making Record Profits in a Global Market Downturn

Faced with an unprecedented imbalance of supply and demand for crude oil, amid COVID-19 and the OPEC+ fallout, traders have ...

Read More

Read More

Hemp Market Reports with PanXchange

RJ Hopp, Director of Hemp Markets at PanXchange, spoke with Kristina Etter, editor of Cannabis Tech, in the first episode ...

Read More

Read More

Physicals, Futures, & Forwards. Know Your Nomenclature

Futures, forwards, cash markets, spot markets, derivatives…. Let’s get the lingo right and get to some more sophisticated price risk ...

Read More

Read More

Q&A: COVID-19 Brings More Uncertainty to an Uncertain Crop

The “building its ship as it sails” hemp industry is no stranger to operating amidst uncertainty – and it’s probably ...

Read More

Read More

Benzinga Summary of PanXchange’s March Hemp Report

The firm covered various topics ranging from regional spot prices (biomass, crude oil, distillate, and isolate), to legislative updates such ...

Read More

Read More

Industry Leaders Discuss The Evolution of the ‘Green Rush’

Attesting to speaker quality and experience, over 80% had PHD’s. This year a Quality Summit was added to address important ...

Read More

Read More

Hemp Suppliers at Odds With Hazy Regulations

Farmers cheered when hemp was legalized nationally for the first time in decades. But more than a year later, differing ...

Read More

Read More

Hemp Barons 0050: Julie Lerner | PanXchange

Hemp buyers and sellers face a number of challenges, some are the result of prior regulatory concerns and some are ...

Read More

Read More

Tumbling Hemp Prices: Good for Consumers, but Bad for Business

Hemp prices have fallen some 80 percent since summer highs as the industry works through a glut of the crop ...

Read More

Read More

Hemp farmers should act fast to sign up for new USDA crop insurance options

Federal agriculture officials have introduced two crop insurance programs for hemp, both designed to protect farmers growing the new commodity ...

Read More

Read More

Hemp Biomass Crop Insurance and Price Risk- How to forward sell with @PanXchange

On February 6th, 2020, the USDA released details of three types of crop insurance for US growers of industrial hemp. This ...

Read More

Read More

Over-Hyped Hemp? Amid Price Drop And A Big Bankruptcy, Some Farmers Feel Burned

It’s an overcast January day on his farm in west Kentucky, where he grew 18 acres of hemp last year, ...

Read More

Read More

Hemp prices plunge as CBD demand falls short

NEW YORK — It may not be apparent when you’re spending $70 on CBD foot cream, but hemp prices are ...

Read More

Read More

Top 10 Trading Solution Companies – 2019

The capital markets industry is intertwined with technology in an ambitious bid to update legacy systems, improve cybersecurity and enhance ...

Read More

Read More

Hemp Prices Plunge as CBD Demand Falls Short: Cannabis Weekly

It may not be apparent when you’re spending $70 on CBD foot cream, but hemp prices are plunging amid a “grossly oversupplied” market, ...

Read More

Read More

Bloomberg: “What’d You Miss?”

PanXchange Founder & CEO, Julie Lerner, talking on 'What'd You Miss?' regarding the Future of Hemp Trading and the Opportunities ...

Read More

Read More

What the Hemp Industry could look like in 2020

According to the PanXchange, there is an issue of massive oversupply in the hemp market. PanXchange Founder and CEO Julie ...

Read More

Read More

Looking Ahead to the Commodities Market in the Hemp Industry: Q&A with Andrew Graves

The hemp market continues to settle as farmers look to the 2020 season. As U.S. growers learn from lessons they ...

Read More

Read More

Hemp Prices Crash, Leaving Ohio Valley Farmers Feeling Burned

Ohio Valley farmers planted more than 27,000 acres of hemp last year — about four times more than in 2018 ...

Read More

Read More

U.S. hemp ‘grossly oversupplied’ – and pressuring CBD prices: PanXchange

The oversupply of U.S. hemp, which was largely grown last year for CBD extraction, could be significantly bigger than expected ...

Read More

Read More

5 Questions about USDA Hemp Regulations with PanXchange CEO Julie Lerner

We talked with PanXchange’s CEO Julie Lerner to get an insider’s view on what the proposed regulations mean to this ...

Read More

Read More

The Week In Cannabis: Illinois Goes Rec, Quebec Pulls Back And A Recap Of 2019

Legal cannabis for adult use arrived to Illinois, with long lines outside of dispensaries formed on Jan 1. The day ...

Read More

Read More

For many U.S. farmers who planted hemp, CBD boom leaves bitter taste

Dan Maclure planted eight acres of hemp on his Vermont farm for the first time this year, aiming to cash ...

Read More

Read More

Rocky start for inaugural hemp auction, but more events are planned

Optimism around a three-day hemp auction in Tennessee turned to disappointment when producers found way more sellers than buyers, driving ...

Read More

Read More

Marketplace Exchanges Offer Hemp Farmers Harvest-Saving Opportunities

Passage of the 2018 Farm Bill and the rise of CBD as a nutritional supplement has led to a boom ...

Read More

Read More

Lessons learned from Colorado’s first hemp harvest since legalization

It’s the first harvest season since the 2018 U.S. Farm Bill was signed into law — and hemp farmers, investors and analysts ...

Read More

Read More

Farmers Start to Get High on Hemp

After years of falling crop prices, some farmers see a lifeline in hemp.Thanks to recent changes in federal legislation, hemp, ...

Read More

Read More

U.S. hemp harvest brings hope to some farmers, heartbreak to others

DENVER, Oct. 3 (UPI) -- A glut of CBD oil on the market, severe weather and a complex harvesting process ...

Read More

Read More

Best Pricing & Valuations Data Provider

We are thrilled to announce that @PanXchange has been shortlisted in the Best Pricing & Valuations Data Provider category at ...

Read More

Read More

How to Capitalize on Emerging Trends in the Legal U.S. Hemp Market

How to Capitalize on Emerging Trends in the Legal U.S. Hemp Market, led by PanXchange CEO Julie Lerner and PanXchange ...

Read More

Read More

From Grains to Frac Sand to Hemp

If you had told Julie Lerner eight years ago that the commodity trading platform PanXchange, which she was building with ...

Read More

Read More

PanXchange Launches Industry’s First Hemp Exchange

August 1, 2019 – PanXchange, a physical commodities OTC market structure solutions provider, today announced the launch of the industry’s ...

Read More

Read More

PanXchange Frac Sand Market Data Now Available on Quandl

Denver, June 13, 2019 -- PanXchange, an OTC exchange and price discovery platform for physical commodities, today announced that it ...

Read More

Read More

Hemp Value Extraction

The majority of CBD is extracted from hemp through two main processes: CO2 extraction and solvent extraction.CO2 extractionIn this process, ...

Read More

Read More

Post Harvest Processing

As hemp crops in the ground begin to mature, we’ve been continually asked by producers what’s going to happen to ...

Read More

Read More

PanXchange Adds S&P Global Platts Veteran Andy Bose to Board of Advisors

Denver, May 09, 2019 (GLOBE NEWSWIRE) -- PanXchange, an OTC physical commodity exchange and price discovery platform for products including ...

Read More

Read More

New Commodity Exchange Platform PanXchange Set To Revolutionize The Hemp Industry

The hemp industry is set to see significant changes in the coming years with the passing of 2018s Farm Bill, ...

Read More

Read More

Denver Business Journal: Nation’s first hemp index by PanXchange aims to drive standardization of market

Denver-based online commodities trading platform PanXchange is stepping up — implementing a price-discovery system and report meant to create transparency in what has effectively ...

Read More

Read More

What Is Hemp?

Hemp is a member of the cannabis sativa family but differs from marijuana as hemp is cultivated for an array ...

Read More

Read More

Cargill and Heifer launch Hatching Hope Global Initiative to improve nutrition and bolster livelihoods of 100 million people

Full Press Release WASHINGTON, March 21, 2019 /PRNewswire/ -- Cargill and Heifer International have joined forces to create The Hatching Hope ...

Read More

Read More

PanXchange and CQG Announce Market Data Partnership

Find full press release here. DENVER, March 13, 2019 /PRNewswire/ -- PanXchange, a Denver-based OTC physical commodity exchange and price ...

Read More

Read More

PanXchange Launches Industrial Hemp Pricing

PanXchange, a Denver-based OTC physical commodity exchange and price reporting provider, today successfully launched its industrial hemp indices, becoming the ...

Read More

Read More

Most Admired CEO Julie Lerner Disrupting Commodity Trading

Julie Lerner founded PanXchange in 2011, launching with minimal investment the first company to bring the negotiation and trade of ...

Read More

Read More

PanXchange Celebrates Anniversary of Frac Sand Launch

This month, PanXchange (PX), a Denver-based OTC physical commodity exchange and a market structure solutions provider, marks its one year ...

Read More

Read More

PanXchange Recognized as One of the “Top 10 Trading Solution Providers- 2018”

Capital Markets CIO Outlook has named PanXchange one of the Top 10 Trading Solution Providers of 2018. Take a look ...

Read More

Read More

Julie Lerner – Denver Business Journal

The Denver Business Journal celebrated 20 years of impactful women by recognizing influential leaders and innovators in the business community ...

Read More

Read More

Julie Lerner Appears on Anthony Crudele’s Futures Radio Show

“Futures Radio Show, hosted by Anthony Crudele, welcomed Julie Lerner to discuss her background in commodities, her opinions on derivatives ...

Read More

Read More

Blockchain for Physical Commodity Markets – A Realist Perspective

People are excited about blockchain. They believe it will solve inefficiencies in everything from stocks and bonds to production and ...

Read More

Read More

PanXchange Places First at Barchart Fintech Exchange

We are pleased to announce that PanXchange placed first at the Barchart Fintech Exchange competition in Chicago last week. Sixteen companies from ...

Read More

Read More

Shifting Sands: Prices, Supply, Demand Concerns Remain in Permian

Julie Lerner experienced what she described as a moment reminiscent of an American television drama series while attending a recently ...

Read More

Read More

PanXchange Enters U.S. Market with Designs on Simplifying Movement of Frac Sand

The enormity of the trucking industry can be realized by looking at the myriad of industries that depend on freight ...

Read More

Read More

Going Local for Supplies Sparks New Frac Sand Boom

Windblown dunes in west Texas are the latest front in the shale oil industry’s campaign to extract more barrels at ...

Read More

Read More

PanXchange Quarter 4 Updates

PanXchange has first-mover advantage in sand as the industry grows by an estimated 30 million tons from 2017 to 2018. It ...

Read More

Read More

PanXchange Frac Sand Launch Schedule

It's here! The first US open market exchange for frac sand will go live on October 4th, 2017. ...

Read More

Read More

Frac Sand: Raw Material or Fungible Commodity?

Since its first pilot launch in world market sugar, the PanXchange team has researched many different commodity markets, seeking to ...

Read More

Read More

Julie Lerner Speaks at MarketsWiki Education’s World of Opportunity

On July 21st, CEO and founder of PanXchange, Julie Lerner, spoke at MarketsWiki Education's World of Opportunity event in Chicago, ...

Read More

Read More

PanXchange Opens London Stock Exchange

Today London Stock Exchange welcomes UK’s Department for International Trade (DIT) and their USA FinTech Mission to the UK. Seven top financial ...

Read More

Read More

The Commodities Disruptor

It was 3 a.m., and the warm Kenyan air smelled of jet fuel. Julie Lerner had just completed a 36-hour ...

Read More

Read More

PanXchange and Bulkloads Announce Strategic Alliance

Denver, CO and Nixa, MO. October 10, 2016. PanXchange, Inc, an electronic negotiation and trading platform for physical commodities, and ...

Read More

Read More

PanXchange Named as Innovator of 2016, by Futures Industry Association

PanXchange has been selected to the FIA Innovators Pavilion, for their 32nd annual Futures and Options Expo, from October 18th through ...

Read More

Read More

Hillary Clinton Visits PanXchange During First Week of US Feed Grains Trading at PanXchange

Denver, Colorado. June 28, 2016 U.S. Democratic presidential candidate Hillary Clinton visited with the team from PanXchange, Inc., a web-based ...

Read More

Read More

PanXchange Inc. Opens Pilot Launch for US Feed Ingredients with 15 National Companies and 35 Traders

PanXchange (PX), a web-based software for the negotiation and trade of physical commodities opened its pilot launch to select US ...

Read More

Read More

PanXchange Launches U.S. Feed Ingredients Pilot

PanXchange (PX), web-based software for the negotiation and trade of physical commodities, opened June 27 its pilot launch to select ...

Read More

Read More

PXAfrica Launches Into World Wheat Market, Grows 150% Since Launch

NAIROBI, KE -- 03/09/16 -- PXAfrica Ltd, a subsidiary of PanXchange, Inc., reached two new milestones this week, the first of which ...

Read More

Read More

Food, Farms, and Forests: The Chaos of Fear and High Expectations

We have grave concerns in today’s world agricultural commodity markets, and I’m not speaking of trade houses’ shrinking profit margins. There’s fear ...

Read More

Read More

PXAfrica Grows 85% in Two Months, Establishes a Liquid Market Less than 90 Days from Launch

NAIROBI, KE, November 05, 2015 - PXAfrica Ltd, a subsidiary of PanXchange, Inc., celebrated the end of its second full month with ...

Read More

Read More

Tough Questions About Financial Sustainability

On the heels of a successful pilot, August will mark my third trip to Kenya and the live launch of ...

Read More

Read More

East African Grain Market Embraces PanXchange’s Live Launch of PXAfrica

PXAfrica Ltd, a subsidiary of PanXchange, Inc., celebrated the end of its second week with live negotiations of maize and ...

Read More

Read More

Transparency and Physical Commodity Markets: It Doesn’t Need to be Complicated

To a physical commodities trader, Eddy Murphy’s down-and-out character in 1983’s film “Trading Places” became a futures trader, a speculator, ...

Read More

Read More

PanXchange Concludes Successful Pilot Launch for Web-Based Grain Trading in East Africa

October 16, 2014. Denver, CO. PanXchange concluded a successful pilot launch for the online negotiation and matching of physical maize ...

Read More

Read More

PanXchange Launches East African Grain Trading Platform

On July 8, 2014, PanXchange launched the pilot of its East African grain trading platform. Through a contract with USAID Firm, ...

Read More

Read More